Written By Zane Willman, Associate Advisor | CCG Real Estate Advisors

If you own a condo as an investment property, you might be asking yourself a crucial question:

Is it actually working as hard as it could for your portfolio?

While condos offer an accessible entry point into real estate investing, they often come with hidden expenses and limitations that can quietly erode your returns over time.

Let's break down how condos actually stack up as an investment and how it compares against multifamily properties—for your long-term wealth.

The Monthly Expense Reality Check

When you own a condo, your monthly obligations extend well beyond your mortgage payment.

You're typically facing HOA fees that can range from $200 to $800 or more per month, depending on your location and amenities. These fees cover building maintenance, insurance, landscaping, and common areas—but here's the catch: you have zero control over when they increase. HOA boards can vote to raise fees at any time, and these increases directly impact your bottom line.

With a multifamily property—let's say a fourplex or small apartment building—you're responsible for the entire maintenance budget, but you also have full control over the outcome. You decide when to upgrade, which vendors to use, and how to allocate resources. More importantly, you can spread major expenses across multiple rental incomes. If you need to replace a water heater in one unit of your fourplex, the other three units are still generating cash flow to help cover expenses.

Property taxes are another consideration. While both condos and multifamily properties are subject to property tax, multifamily buildings are assessed differently and often benefit from commercial property tax treatment, which can include various deductions and depreciation benefits that individual condo owners don't typically access.

Cash Flow: The Numbers Tell a Different Story

Let's paint a realistic picture.

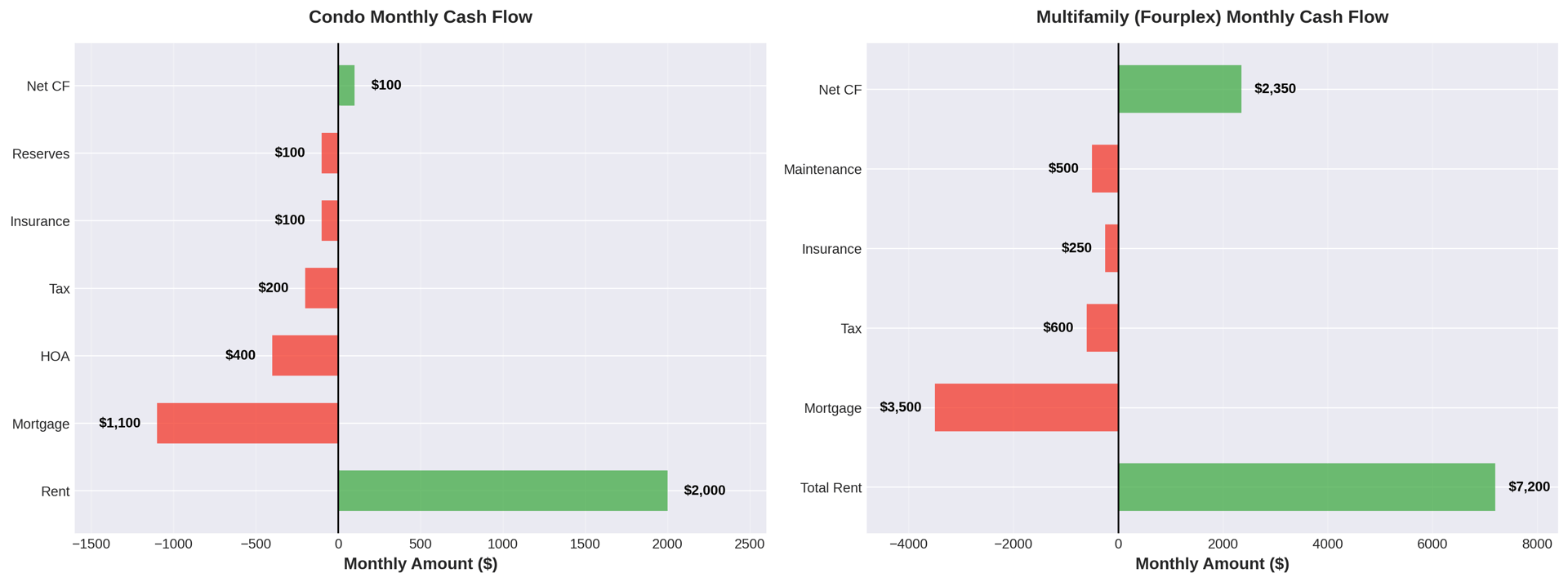

Imagine you own a condo that rents for $2,000 per month.

After your mortgage ($1,100), HOA fees (-$400), property tax (-$200), insurance (-$100), and setting aside reserves for maintenance (-$100), you're netting about $100 per month—or $1,200 per year.

That's before accounting for vacancy, which averages 5-8% annually in most markets.

Now consider a fourplex where each unit rents for $2,000/mo. Your total gross rental income is $8,000 monthly.

Even with a larger mortgage (-$3,500), property tax (-$600), insurance (-$250), and maintenance (-$500), you're still clearing roughly $2,350 per month—or $28,200 annually. The key difference? Income diversification. If one tenant moves out, you've only lost 25% of your income, not 100%.

This diversification becomes even more powerful when you consider tenant turnover costs. With a condo, every vacancy means zero income until you find a new tenant. With multifamily, you maintain cash flow while filling vacancies, and you can often stagger lease renewals to avoid multiple simultaneous turnovers or renovations.

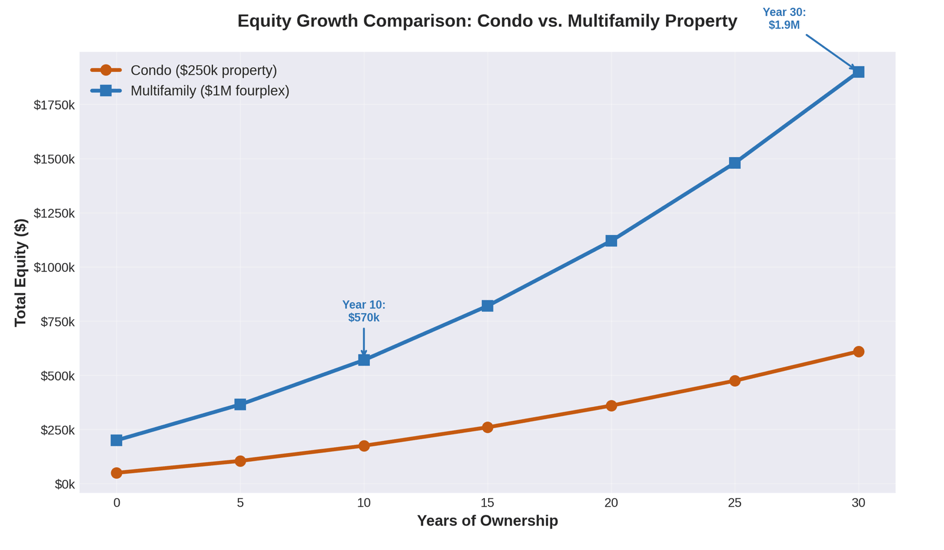

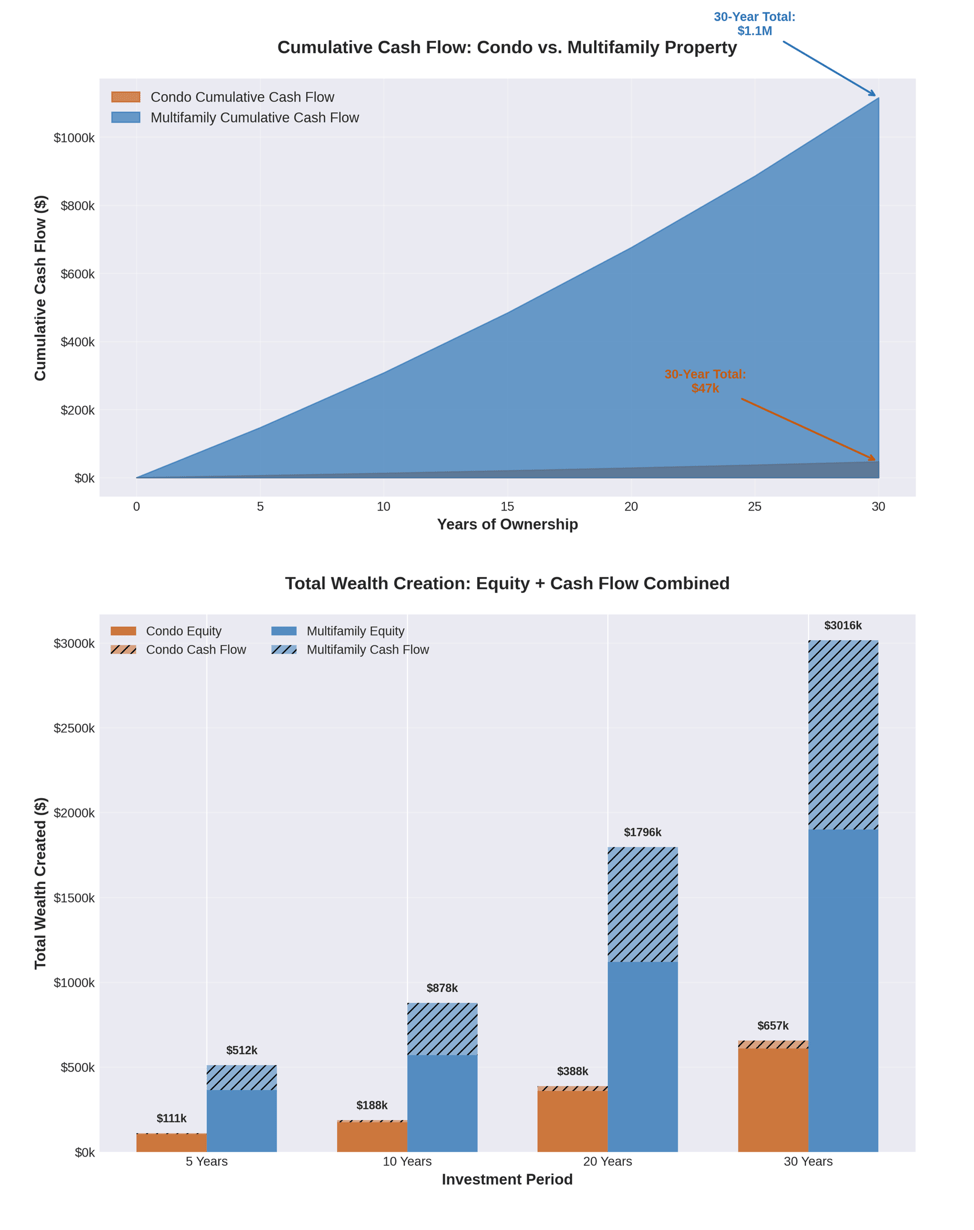

Compound Growth Over Time: Where the Real Wealth Lives

The true power of real estate investing happens over decades. Let's see how your equity compounds differently between a condo and a multifamily property over 5, 10, and 30 years.

- Year 5:

- After five years of ownership, your condo has appreciated at perhaps 3% annually (depends on the market), and you've paid down a modest amount of principal. You might have gained $40,000 in equity from appreciation and another $15,000 from loan paydown—about $55,000 total.

- Meanwhile, your fourplex, which started at a higher basis but also appreciates, has gained $120,000 in appreciation across all four units plus $45,000 in principal paydown. Crucially, that annual $28,200 in cash flow has also generated an additional $141,000 in cash reserves over five years, assuming you've been banking it.

- Year 10: The gap widens

- Your condo equity might total $130,000 from appreciation and principal reduction combined.

- The multifamily property, benefiting from forced appreciation through rent increases and operational improvements you control, could be worth $350,000 more than your purchase price, plus another $95,000 in principal paydown. Your cumulative cash flow has now exceeded $300,000, which you could have used to invest in additional properties.

- Year 30: This is where the truly transformative wealth gap appears.

- Your paid-off condo is now worth perhaps $450,000 (from an original $250,000 purchase), and it generates $2,000 monthly in mostly passive income.

- Your paid-off multifamily property is now worth $1.8 million and generates $8,000 monthly. Over 30 years, the multifamily property has produced over $900,000 in total cash flow—money you could have reinvested into additional properties, creating exponential portfolio growth.

Performance During Economic Downturns

Perhaps the most important consideration for any investor is resilience during recessions. Historical data from the 2008 financial crisis reveals telling patterns about how different property types weather economic storms.

During the Great Recession, condos in markets like San Francisco saw price declines of approximately 12%, while single-family homes dropped 19%. However, this doesn't tell the full story. Luxury condos and new construction condos in oversupplied markets like Miami experienced much steeper declines—some falling 40-50% from peak values. The condo market also took longer to recover in many areas, with some markets not returning to pre-recession prices until 2013 or later.

Multifamily properties, by contrast, demonstrated remarkable resilience. While multifamily property values initially dropped 40% from peak to trough between 2007 and 2009, they rebounded 20% by the end of 2010 and fully recovered faster than most other real estate sectors. Why? Because during recessions, rental demand actually increases. Tighter lending standards, job uncertainty, and foreclosures push more people into the rental market. Even if rent growth slows, occupancy rates in multifamily properties typically remain stable or even improve.

Here's the critical distinction: multifamily properties, especially workforce housing (Class B and C buildings), benefit from countercyclical demand. When the economy struggles, people still need housing—in fact, they need affordable rental housing more than ever. Luxury condos, on the other hand, often see demand evaporate during downturns as buyers and renters downsize or postpone purchases.

The income diversification of multifamily properties also provides a crucial buffer. If you own a fourplex during a recession and lose one tenant, you retain 75% of your income. If you own a condo and your tenant leaves, you have zero income until you find a replacement. While still owing your full mortgage, HOA fees, and property tax, those expenses stack up and could end up costing you money than actually making any.

Making the Strategic Decision for Your Portfolio

There's a saying in real estate: "Friends don't let friends buy condos". For some investors—particularly those just starting out, living in high-barrier-to-entry markets, condos can serve a purpose. However, the key is understanding what you're getting and what you're giving up.

If your condo is barely breaking even or losing money after all expenses, it might be time to ask whether that capital could work harder for you in a multifamily property. If you're tired of HOA fee increases you can't control, or if you want to build true generational wealth through real estate, multifamily properties offer a path that condos simply can't match.

The choice ultimately comes down to your goals. Are you building a real estate portfolio designed for long-term wealth accumulation, cash flow, and economic resilience? Or are you looking for a more hands-off investment that requires less initial capital and management oversight?

If you're ready to take your real estate investing to the next level, understanding these fundamental differences is the first step toward making a strategic move that could transform your financial future.